By Richard Owen & Maurice FitzGerald

Field Notes on Customer AI · Edition 005 · May 26, 2026

Each Tuesday, Field Notes surfaces what we're seeing in the field: patterns from implementations, ideas worth stress-testing, and the occasional inconvenient truth about how Customer AI programs succeed or stall. No abstractions. No product pitches. Just the working knowledge that tends to matter.

This edition covers another uncomfortable subject: Your customer base is a portfolio. You're managing it like a to-do list.

The Field Read

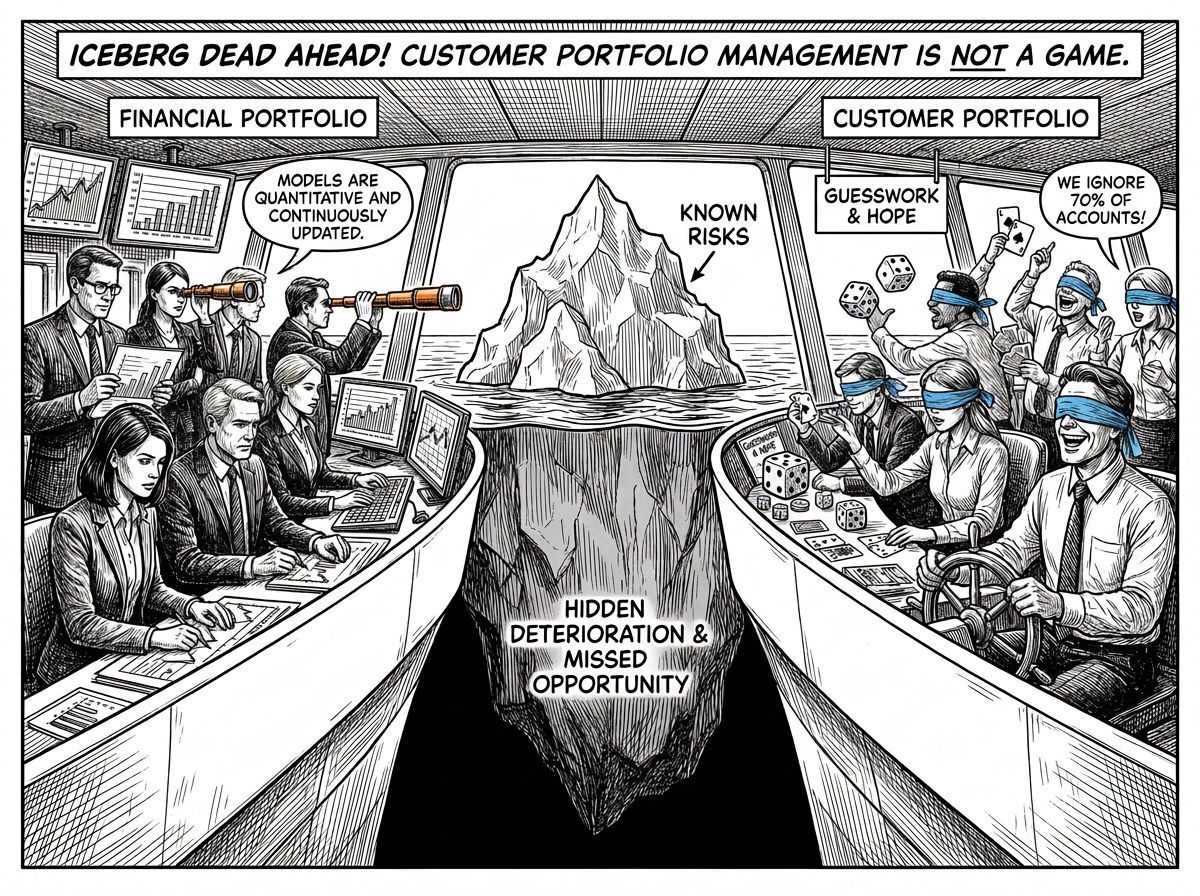

Customer Portfolio Management Is Not a Game - Richard Owen

Fund managers do not guess which holdings to watch. They have models, quantitative and continuously updated, covering every position. They assess risk, identify upside, and allocate attention where the return on that attention is highest. The idea that a portfolio manager would rigorously analyze thirty percent of their holdings and simply hope the other seventy percent were fine would be career-ending. Regulators would be involved.

Yet this is essentially how most companies manage their customer base. The installed customer base is, in most enterprises, the single largest determinant of financial performance. It is managed with dramatically less analytical rigor than a financial portfolio one-tenth its economic value. Not because leaders do not care. Because, until recently, the tools to provide portfolio-level intelligence about customers simply did not exist.

The risk side of this equation is expensive. Every customer portfolio contains accounts that are quietly deteriorating: usage declining, engagement thinning, the relationship cooling. None of the conventional alarms go off. Health scores, where they exist, are typically constructed from indicators weighted by committee consensus rather than validated against actual outcomes. A weather report and a weather forecast are not the same thing, and the difference between them is measured in lost revenue.

The opportunity side is arguably worse, because you cannot mourn revenue you never knew was there. It costs five to six times more to acquire a dollar from a new customer than to expand an existing one. Yet resource allocation in most organizations still tilts heavily toward new logo acquisition. Companies with dedicated expansion motions achieve twenty-eight percent higher net retention than those focused solely on keeping what they have. The arithmetic is not complicated. The execution gap is where the money disappears.

The discipline required is the same one that financial portfolio management takes for granted: continuous assessment of every position, with attention allocated to where it changes outcomes rather than where it follows the calendar or the loudest voice.

[Read the full article: "Customer Portfolio Management Is Not a Game" → Here]

The Practitioner's Take

The question nobody asked about our happiest customer - Maurice FitzGerald

At HP, the entire CX operating model was designed around one word: fix. Fix the escalations. Close the loop with Detractors. Respond to complaints. Run to the fire.

We were good at it. What we never asked was the other question: what are our happiest customers doing differently, and how do we help more customers do the same? The Promoters, the customers who scored nine or ten, were treated as a success story to mention in a quarterly slide. Nobody was mining them for growth signals. Nobody was asking which product combinations, which onboarding patterns, which account team behaviors produced those scores, and then replicating them across the base.

The growth opportunity was sitting in the NPS data the whole time. We never built a system to see it, because the system was designed to find problems, not to find patterns.

So therefore: look at your top twenty Promoter accounts. Ask what they have in common: adoption patterns, engagement rhythms, commercial trajectory. If nobody in your organization can answer that question today, you are managing only the risk half of your customer portfolio. The opportunity half is invisible.

The Field Tactic

Three Ways to Stop Managing by Rear-View Mirror

Three ways to manage the portfolio, not just the problems:

- Score for opportunity, not just risk. Take your top fifty accounts and rank them by expansion readiness: product adoption depth, usage growth trajectory, executive engagement strength. If your current system can only flag accounts at risk and cannot identify accounts ready to grow, your intelligence covers half the portfolio at best.

- Run the Soames test. Pick five accounts and plot them on two axes: financial performance and customer sentiment. Any account with strong financials and weak loyalty is borrowing from the future. Any account with strong loyalty and weak commercials is an unrealized asset. Both need different interventions, and neither is visible through a single metric.

- Calculate your expansion gap. Compare your current net revenue retention to best-in-class performance of 120% or better. Multiply the difference by your ARR. That number is the expansion revenue sitting unrealized in your installed base each year. Put it in front of your CFO. The conversation tends to be clarifying, to say the least.

The Data Point

The number - the $0.27 growth engine:

$0.27 versus $1.16

That is the cost to acquire one dollar of contract value from an existing customer through upsell, compared to one dollar from a new customer, according to Pacific Crest's SaaS survey. Expansion through plan growth is even cheaper: $0.20 per dollar. The cost advantage is five to six times.

More recent data from Benchmarkit confirms the gap is widening. The new-customer CAC ratio reached $2.00 in 2024, while the blended ratio including expansion remains materially lower. The installed base is, by the numbers, the most capital-efficient growth engine most companies have. It is also the one they invest the least intelligence in managing.

Source: Pacific Crest SaaS Survey; Benchmarkit (2024)

The Iconoclast Question

The Other Half of the Portfolio

What percentage of your customer success team's time goes to accounts that are already at risk, versus accounts that are ready to grow? If the ratio is heavily skewed toward fire-fighting, who is responsible for the expansion revenue nobody is chasing?

The Field Bridge

The Customer AI Masterclass covers portfolio-level customer intelligence: risk, expansion, and where to allocate attention. Module 6 is where the subect starts.

[ Get Certified → $500 off through May 31, use code LEADER500]

Coming in Future Editions

- Prevention Economics.

- Bad Survey Data or Pure Guesswork? A Better Solution to Both.

- Why NPS was never enough, and what replaces it.

- The Executive Sponsorship issue.

If you've been reading Field Notes, you know the problem isn't awareness - it's execution. Knowing that AI can improve retention or accelerate revenue doesn't tell you how to make it happen in your organisation. That's exactly the gap The Customer AI Field Guide was written to close. Authored by Richard Owen and Maurice FitzGerald (that's us), it's a practical execution guide for CX, CS, and RevOps leaders, covering how to identify at-risk accounts before they signal churn, convert customer insights into frontline action, build the financial case that gets CFO sign-off, and design Customer AI systems your teams will actually adopt. Theory optional. Results required.

[ Get the Customer AI Field Guide → Now on Amazon]

Field Notes publishes every Tuesday. Each edition focuses on one topic - a trap, a framework, a field observation, or a pattern worth examining. If something in here resonates, or if you're seeing something different in your own programs, we'd like to hear about it.

Responses